|

Listen to this article

|

Business investment-based US green card program is popular with Indian and Chinese investors to bypass the long queues for their countries in employment and family-based categories.

I have written down the basic rules for EB5 investment here.

Most people are worried about the money needed to file EB5 and how to collect those funds.

I try to list down all possible options for you.

This article will discuss:

How to Collect EB5 Funds

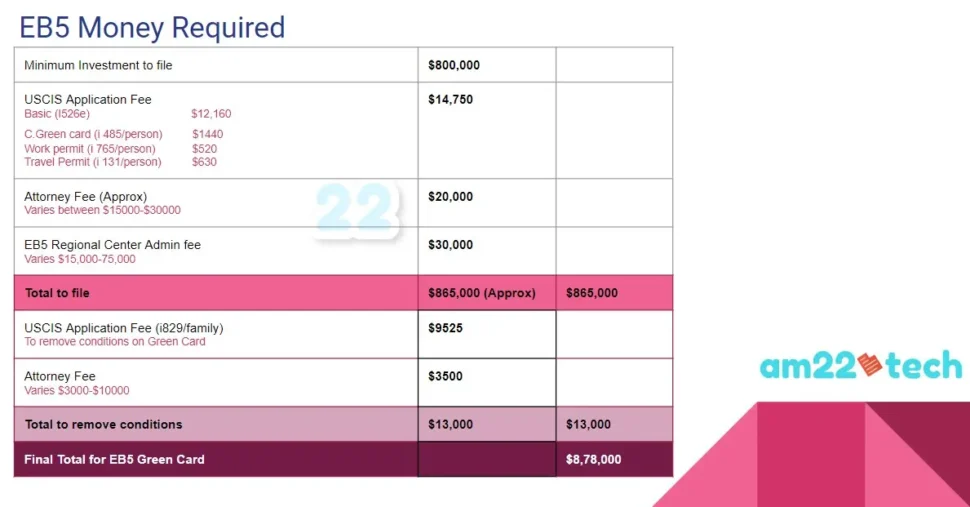

You will need at least $800k to file your EB5 Green card.

Realistically, you will also need an additional $50k to pay for the attorney fee, USCIS fee, and EB5 project admin fee.

Hence, plan for at least 880k to have in hand to take the jump for EB5 investment.

There are various creative ways of collecting funds for your EB5 Investment. We share some of them which are not commonly known to people.

#1 Use 401K Money

You can use your 401k directly as the EB5 investment. The most important thing to understand here is that the project you invest in should be available as the investment in your 401k provider portfolio.

Example:

Many projects make themselves available for investment through the traditional IRA private investment route.

Most employers have big names like Fidelity as their providers. If Fidelity does have your EB5 project as one of their investment options, then you would not be able to invest your 401K money for EB5 purposes.

What’s the solution then?

The solution is to move your 401K money from Fidelity to a provider that has the specific project that you chose for EB5 as an investment option. To find this 401K provider, you can ask the EB5 project’s team as they have all the information.

As an example, the Alto IRA has Behring’s EB5 project listed as an investment.

So, you would need to move your 401K money from Fidelity to Alto IRA to use it as an EB5 investment.

Can I move my 401K to another provider If I am currently working for the same company?

That’s a problem. You can only move the amount of money in your 401K to another provider that is not from your current employer.

This is an IRS rule and has nothing to do with USCIS, Fidelity, or any other 401k Provider.

#2 Roth IRA

You can use the same strategy as we mentioned for 401K above for using your Roth IRA for EB5 investment.

The other method is to withdraw your Roth IRA and use it as cash for the EB5 project.

You will be able to withdraw the Roth IRA amount that you contributed without any tax penalties.

Need Help with EB5 Green Card?

Are you on H1B, H4 EAD, L1, L2 EAD, B1/B2, F1 visa and looking to get green card through EB5?

Total money required for EB5 investment practically?

Processing time for Green card

If you withdraw the growth (the amount that increased due to the market), you will have to pay the penalty and the tax as per withdrawal rules.

#3 EB5 Project Unsecured Loan

Most EB5 project companies also give you an unsecured loan at the market rate.

This can then be used as the EB5 investment in your name to become eligible for the Green card.

You can get a loan of up to 500k for an investment of 800k. You will have to put in your 300k.

This loan follows the market APR rate and is usually 3-4% above the normal APR.

Example 1:

As of the date of writing, the APR for this loan is 11%-18%.

Example 2:

For an EB5 project loan, it is common to pay the interest for the full term of the loan which is 5 years and the principal will be paid by the EB5 developer.

Interest only loan means that you keep paying the interest on the loan monthly and the principal amount stands as it is.

It might be paid by the EB5 regional center or the developer after the completion of the loan term.

Note that if the EB5 business goes down, you will still be liable to pay the EB5 loan principal amount. The financial contract between you and the EB5 loan company will determine what will happen if the EB5 project files bankruptcy.

#4 Money from India/China or Home Country

You can get money from your home country like India or China by selling your assets there.

- Sell Home Country Property – Many people sell their homes or other property to collect money for EB5.

- Mortgage/ Loan on the property – The other way is to take a loan on the property in the Home country and then use it to fund the EB5 project in the USA.

- Borrow from Family & Friends – You can also borrow from relatives, parents, or friends but will need all their proofs of income which may be a little cumbersome to collect.

This is allowed as long as you can prove that money to buy a home was earned legitimately and no taxes are due to the respective home country government.

#5 Other Sources

Whatever sources of money you use, make sure that it is the legitimate source as you will need to submit proof of it.

EB5 Green Card Processing Time

These times can vary but we have provided an estimate based on our understanding.

- EAD & AP:

- 5-6 Months to get EAD for work, 10-12 months to get Advance parole for travel.

- Conditional Green Card:

- Consider 2-6 years based on your EB5 sub-category and the status of your visa bulletin.

- If your EB5 priority date (I526 receipt date) is current in the visa bulletin, then you are eligible for a 2-year conditional green card.

- Your i526 will not be approved until the date gets and remains current.

- Final Green Card

- Your I526 should be approved.

- You will have to apply using the I829 form and request to remove conditions from your conditional green card. This can take several months/years too based on USCIS processing time.

- Citizenship/Naturalization

- Your time on a conditional green card should be counted for your Naturalization/Citizenship but you can’t apply for citizenship until your I829 is approved.

Child Age Protection Using EB5

Your child’s age will be locked when you file I485 with your I526e application.

The child should stay unmarried until they get the greed card though.

FAQ

If you are working on H1B in the USA and have the money to sponsor yourself for the EB5 business investor program, you can apply for an EB5 visa.

I know many people working on H1B and L visas in the USA from India and are actively thinking about investing to get a green card faster than their PERM-based employment green card.

If you have the money for investment, I strongly suggest filing it instead of relying on the bills to remove country-based Green card limits.

USCIS does not allow porting the H1B EB2 priority date to EB5 green card applications.

Unfortunately, you will have to start fresh in the EB5 queue based on your country of birth.

Yes, you can file both and have both EB3 and EB5 applications pending at the same time.

You can withdraw your EB5 I-526 if you get your Green card using any other queue.

The EB5 funds may still be locked in as per your financial deal with the EB5 project company. Note that they usually package everything together and do have a 5-year lock-in to withdraw money. You should read the documents carefully to understand how will you get your money back.

just need to pay the interest for the full term of the loan which is 5 years and principal will be paid by the developer. Is this a common practice or is it too good to be true?

No, you cannot use your personal residence to show as a business investment for the purpose of claiming an EB5 green card.

But, you can take a HELOC (home equity loan) on your residence and then invest it in an EB5 business. This is allowed.

More Questions?

Ask them in the comments and I will try to answer them to the best of my knowledge.